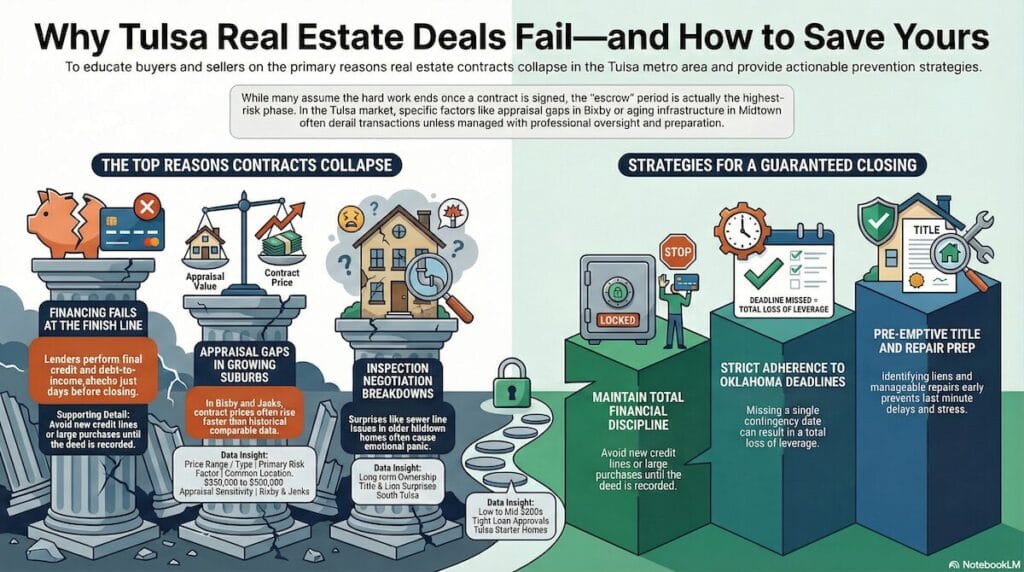

Real estate deals fall through in Tulsa more often than most buyers and sellers expect. Many people assume that once a contract is signed, the hard part is over. In reality, the contract period is where risk is highest. Financing must clear final underwriting, inspections must be negotiated, appraisals must support the price, and strict deadlines must be met.

In Tulsa, Broken Arrow, Bixby, Jenks, Owasso, and surrounding suburbs, every price range carries different contract risks. Starter homes in the low to mid $200s often involve tighter loan approvals. Move-up homes in the $350,000 to $500,000 range frequently face appraisal sensitivity. Downsizing transactions may reveal title complications after decades of ownership. Relocation buyers may struggle with unfamiliar Oklahoma contract timelines.

Deborah Green has managed transactions across the Tulsa metro since the 1990s. Over time, she has seen patterns in why contracts collapse — and more importantly, how to prevent those failures before they escalate. Whether you are buying your first home, coordinating a move-up purchase, downsizing in South Tulsa, or relocating to Jenks, understanding these contract risks gives you leverage and clarity.

The goal is not fear. The goal is preparation. When buyers and sellers understand why contracts fail, they can make decisions calmly and protect both money and timelines.

Key reasons real estate deals fall through in Tulsa, summarized visually.

1. Financing Fails During Final Underwriting

Financing remains the number one reason contracts terminate. Many buyers believe pre-approval guarantees closing, but lenders perform a final verification just before funding. Employment status, debt levels, and credit are reviewed again.

In Tulsa’s starter-home range — typically low to mid $200s — FHA and low-down-payment buyers are especially sensitive to debt-to-income ratios. A small change, such as financing furniture or opening a new credit line, can push ratios beyond lender limits. One Owasso buyer lost approval three days before closing because of a new vehicle purchase.

A common misconception is that lenders “won’t notice” small financial changes. They do. Every inquiry and account adjustment is reviewed before final approval.

This matters because when financing collapses, sellers must relist and buyers lose inspection expenses. Deborah Green prepares clients by reinforcing strict financial discipline during escrow.

For a full breakdown of the process, review Buying a Home in Tulsa.

If you are early in planning, Get the Tulsa first-time homebuyer guide.

2. Appraisals Come in Below Contract Price

Appraisal gaps frequently cause tension in competitive areas like Bixby and Jenks. When contract prices rise faster than closed comparable sales, appraisers may not support the agreed value.

In Broken Arrow’s Battle Creek area, a move-up home priced at $465,000 recently appraised at $445,000 due to limited comparable data. The buyer believed the market justified the price. The lender relied on closed sales.

Why does this happen? Appraisers must use recent, similar sales within defined geographic and size boundaries. In rapidly appreciating neighborhoods, comparable data lags behind contract prices.

Buyers often assume banks will “split the difference.” That rarely happens. Lenders loan based on appraised value.

This matters because appraisal gaps create negotiation pressure. Sellers may reduce prices, buyers may bring cash, or contracts may terminate.

Before pricing aggressively, sellers should check your home’s value (link to property value page) to understand appraisal exposure.

For broader pricing trends, review Tulsa Housing Market & Cost of Living.

Deborah Green discusses appraisal strategy before listing, especially in the $350,000 to $500,000 price range, where sensitivity is highest.

3. Inspection Negotiations Break Down

Inspection surprises frequently derail contracts in Midtown Tulsa and older Jenks neighborhoods. Homes built before 1990 may include aging plumbing, foundation movement, or outdated electrical panels.

In Midtown, sewer line deterioration is common. A buyer may initially love the charm of a 1940s bungalow but panic at a $12,000 estimate for a sewer replacement. Sellers may feel blindsided even if the issue developed over decades.

A misconception is that inspection reports represent mandatory repair lists. They do not. Inspections identify condition, not required fixes.

This matters because emotional reactions escalate quickly. When buyers feel overwhelmed or sellers feel attacked, communication suffers.

Deborah Green encourages sellers to anticipate common Tulsa inspection findings and address manageable repairs before listing.

For seller preparation strategies, review Selling a Home in Tulsa.

4. Title Issues and Long-Term Ownership Surprises

Title problems are less frequent but disruptive. In Tulsa County, unpaid liens, unresolved estates, or recording errors sometimes appear during title searches.

Downsizers in South Tulsa who have owned homes for 25 years may discover unreleased contractor liens. Relocation sellers in Owasso may uncover minor easement disputes.

Many assume long ownership guarantees a clean title. Unfortunately, clerical oversights can persist for decades.

This matters because unresolved title issues can delay closing weeks, impacting rate locks or relocation timelines.

For consumer education, see Understanding the Closing Disclosure.

Deborah Green coordinates early with Tulsa title companies to reduce last-minute surprises.

5. Buyer’s Cold Feet Derail Progress

Not all deals fail due to hard numbers. Some collapse due to fear. First-time buyers in Tulsa may panic after inspection findings. Move-up buyers worry about timing two closings. Relocation buyers question unfamiliar neighborhoods.

In Jenks, a buyer withdrew over minor cosmetic foundation cracks despite the engineer’s clearance. Anxiety overshadowed facts.

Why does this happen? Real estate involves large financial commitments. Without strong guidance, small concerns feel catastrophic.

This matters because emotional decisions can cost thousands in inspection fees and lost opportunities.

To explore areas confidently, review Tulsa Neighborhoods.

Deborah Green emphasizes education early to reduce reactive decisions.

6. Contingency Deadlines Are Missed

Oklahoma contracts include strict timelines for inspections, financing approval, and repair negotiations. Missing a deadline can waive rights.

In Bixby’s new construction, builder addenda often override standard timelines. Relocation buyers unfamiliar with Oklahoma procedures may not realize this.

A common objection is “we can extend it later.” Extensions require agreement from both parties.

This matters because missed deadlines may forfeit earnest money or negotiating leverage.

For buyers exploring builders, review New Construction Homes in the Tulsa Metro.

Deborah Green tracks deadlines proactively across Tulsa metro transactions.

7. Poor Communication Between Parties

Even solid contracts collapse when communication fails. Lenders, inspectors, title officers, and agents must coordinate smoothly.

In a Broken Arrow transaction, lender documentation delays created tension between buyer and seller. The issue was minor, but miscommunication amplified stress.

Many believe only large financial problems kill deals. Often, breakdowns begin with unclear expectations.

This matters because trust determines flexibility during negotiations.

How Deborah Green Prevents Contract Failures in Tulsa

Deborah Green uses structured communication systems across Tulsa, Broken Arrow, Bixby, Jenks, and Owasso. Deadlines are calendared. Lenders are confirmed. Inspection expectations are set in advance. Appraisal risk is discussed before listing.

Prevention is quieter than crisis management — but far more effective.

Frequently Asked Questions

Why do real estate deals fall through in Tulsa after inspection?

Real estate deals in Tulsa fall through after inspection when repair negotiations escalate beyond reasonable expectations. In older neighborhoods like Midtown Tulsa, aging systems often require compromise. With realistic pricing and communication, most inspection issues can be resolved without termination.

Can sellers cancel after a low appraisal?

Sellers typically cannot cancel solely due to a low appraisal unless specific contingencies apply. Instead, price adjustments or gap coverage are negotiated.

Are appraisal gaps common in Bixby and Jenks?

Appraisal gaps occur more often in competitive price bands where contract prices rise faster than closed sales data. Preparation reduces risk.

How can buyers protect earnest money?

Buyers protect earnest money by following contingency timelines precisely and maintaining stable financing during escrow.

Conclusion

Real estate deals fall through in Tulsa for predictable reasons. Financing discipline, realistic pricing, inspection preparation, and structured communication dramatically reduce risk.

Preparation protects time, money, and peace of mind across every price tier in the Tulsa metro area.

If you want to map out a clear strategy before making a move, Schedule a low-pressure planning call.

Planning prevents preventable problems.